AskChristee Mobile App Overview

The Christee mobile app performs calculations in the same manner as the website www.AskChristee.com . The app contains 12 modules where the website contains 16 modules.

For additional information, please visit the ‘Resource’ tab at AskChristee.com

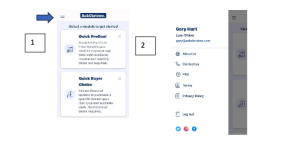

Getting Started. When you open the Christee App, you will see screen ‘1’ which displays the Christee modules. You may also select the menu icon in top left corner to access menu as shown in image ‘2’ below. This documentation will be available in screen # 2.

The arrow in Image 3 below shows the Kabab Menu. Use this menu access help (image 4) file for each module or clear prior input data for the selected module. Otherwise, prior input data is available and can be edited. Help file is available for each module to provide explanation for each required and optional input.

Image ‘5’ below shows option to access the ‘PDF’ file and also ‘Minimum Cash Results’ slide bar. Image ‘6’ shows the bottom of input screen. Please note the green circle with check inside – this is the submit button to receive results report. Additionally, on the input page under ‘Optional

Inputs’ you have the option to enter a name which will appear on the PDF file. You may also change the email address for sending the ‘PDF’ file – the default setting is the email address associated with your login credentials.

Basic Concepts and Terms Associated with Christee Reports.

Target Payment. An affordable home price is based upon a target monthly payment, available cash, and loan type. An affordable target payment is based on credit score, income, monthly debts, qualifying ratios, and loan type.

Note. Relax Christee does all the calculations. Even in module that require input of income, user may enter the desired monthly payment.

Cash. Available cash for closing cost and downpayment is critical in determining an affordable purchase price. Required cash will be influenced by two factors – location and loan type. If available cash is not entered Christee will resolve the ‘target payment’ to a purchase price and minimum cash required.

Example. A $3,500 target payment would allow for the purchase of a $431,231 home. The minimum downpayment is $15,094 (3.5%) and closing cost are estimated to be $16,230 for total minimum cash required of $31,324. Closing cost will vary based upon location of the property.

Minimum Cash Required. The above example illustrates ‘Minimum Cash Results’. In other words, what is the max price home based upon ‘Target Payment’ and how much total cash is required including closing cost. This is referred to as ‘Minimum Cash Required’

Available Cash. If the available cash is greater than minimum cash, Christee will show a higher purchase price while maintaining the target monthly payment. If the available cash is less than minimum cash then the purchase price will be adjusted to spend available. This is referred to as ‘Spending Cash Option’.

Note. Enter Cash in the optional inputs drop down.

Note. Required cash may be lowered by seller or lender credit, whereas required cash will be increased by lender fees and/or loan origination fees. See below.

Loan Type. The loan type selected will influence purchase price and required cash. In most modules you may select any combination of loan types – Conventional, FHA, VA, or USDA. If you are unfamiliar with these loan types, please visit the resource tab at www.AskChristee.com.

Note. Relax, you only need to understand the basics. Christee will perform all the calculations and provide additional insights in the notes section for each report.

Seller Credits. Sellers may pay all or part of buyers’ closing cost thus reducing amount of required cash which may dramatically increase potential purchase price. Each loan caps the amount of seller contributions or concessions. Christee will adjust credits based upon loan type. Enter Seller Credits in optional inputs.

Lender Credits. Lenders may contribute to buyers’ closing cost. Typically, this will result in a slightly higher interest rate. Enter lender credits in optional inputs.

Lender Fees. It is not uncommon for lenders to have fees such as processing, administrative, or underwriting to name a few. These fees will increase closing cost and enter them under optional inputs.

Origination Fees. A fee (prepaid interest) in exchange for a lower interest rate for the loan term. Origination fees increase closing cost and are based upon loan amount. Enter any origination fee under optional inputs.

Subsidy or Buydown. A subsidy or temporary buydown lowers the monthly payment for a fixed period – typically one, two, or three years. In ‘optional inputs’, select buydown. Available for Buyer PreQual and Buyer Choice Modules.

Qualifying Ratios. Lenders develop Qualifying Ratios. One of these ratios is the mortgage payment plus debts expressed as a percentage of gross monthly income known as Debt-to-Income ratio or DTI. While this ratio is important in the approval process, it may not be definitive. Additionally, allowable DTI is different for each loan type and Lenders may differ on allowable DTI ratios.

Note. Christee will display the DTI ratio when income is entered.

Tax Considerations. A homeowner is entitled to reduce their taxable income by mortgage interest and property taxes. Christee will display estimated amount of tax deduction for all modules. Potential tax savings will be displayed for modules where income is entered.

Understanding Christee Notes.

Each Christee report will include a brief note section for each loan type selected. Below is a brief explanation for typical notes. You may also consult ‘Help File’ associated with each module.

Generic Notes Applicable to all loan types.

Loan notes will vary depending upon the module executed and other circumstances.

Buydown. Will indicate that a temporary payment buydown would lower payment. This is useful in times of higher interest rates. Seller can pay cost of buydown as part of seller concession limitations. Not applicable to USDA loans.

Limit Payment. A reminder in certain modules you can control the ‘Target Payment’ with optional input ‘Limit Payment’

Max Seller Credits. Christee will indicate maximum seller credit or inform you that maximum seller credits have been used.

Notes for Conventional Loans

Conforming / Jumbo Loan. Christee will indicate if the loan amount exceeds conforming loan amount and is considered a ‘Jumbo’ loan. Jumbo loans have higher interest rates and are based on location.

Home Ready Program. The Home Ready Program offers benefits to buyers who have income in accordance with the Area Medium Income (AMI). Benefits include acceptance of lower credit score and reduced downpayment requirements. Minimum downpayment will be adjusted with suggestion you discuss Home Ready or Home Possible Program with Lender.

PMI. Private mortgage insurance is required on conventional loans with less than a 20% downpayment. The notes will indicate the necessity of PMI.

Note. You can turn off calculation of PMI in optional inputs. This should be done with extreme caution and consultation with loan officers.

FHA Notes.

FHA Limit. The maximum FHA loan amount is based upon location of the property. You will alerted when loan amount is capped by FHA limit.

UFMIP and Monthly MIP. Christee will include applicable Up Front Mortgage Insurance (UFMIP) and Monthly Mortgage Insurance (MMI) with all FHA reports. Results display will include base loan amount (max 96.5% of sales price) and UFMIP displayed as part of Total Loan Amount.

VA Notes

VA Conforming/ Jumbo. Alert as to whether loan amount is conforming or Jumbo. Jumbo loan amounts require higher interest rate.

Funding Fee. All VA loans are subject to an upfront funding fee (except exempt Veterans). The Funding fee is added to base loan amount for total loan amount. The funding fee is based upon loan LTV and whether this first VA loan for the veteran. Under optional inputs, you can select Exempt or First VA loan.

USDA Notes.

USDA Availability. USDA loans are only available in certain locations – typically not Urban areas. Christee will alert you as to whether (a) USDA loans are completely available (b) partially available (c) Not available in area.

Mortgage Insurance. All USDA loans require monthly mortgage insurance and is included in total payment calculations.

USDA Income Limitations. USDA borrowers are subject to maximum household income restrictions. Christee will display this amount to review with a loan officer.

USDA MAX LTV. USDA loans allow for 100% financing or zero downpayment.

Funding Fee. USDA loans require a ‘Funding Fee’ which is included in total loan amount.

Module Explanation.

There are 12 modules available in the Christee Mobile app. Below is a brief overview for each module.

1. Quick PreQual. Easily convert a ‘desired monthly mortgage’ payment into a projected purchase price based upon loan type(s) and location. Report includes closing cost, downpayment and total cash required, total monthly payment and potential tax deduction. There is a menu of optional inputs to customize the report.

Note: Best suited for consumer or real estate agent when buyers’ income is unknown.

2. Quick Buyer Choice. Quickly develop potential purchasing scenarios for a specific price property based on loan type, cash, and desired monthly payment. The report will include required cash including downpayment and closing cost plus a breakdown of the monthly payment and potential tax deduction. A variety of optional inputs allow you customize report.

Note: Best suited for consumer or real estate agent when buyers’ income is unknown.

3. Buyer PreQual. Develop a strategy for an affordable home price and best loan type based upon annual income, monthly debts, credit score, and cash for downpayment and closing cost. Christee will suggest an affordable payment for each loan type; however, you may edit the desired monthly payment under optional inputs. There are a host of optional inputs for complete personalized report.

Note. Best suited for curious consumers, smart real estate agents, or loan officers.

4. Buyer Choice. Develops best options for purchasing a specific property based upon annual income, monthly debts, credit score, loan type, and available cash for closing cost and downpayment. Christee algorithms will suggest a monthly payment and loan amount; however, you may override with optional inputs.

Note: Best suited for curious consumers, smart real estate agents, or loan officers.

5. Closing Cost. Explore details of closing cost based upon location, purchase price, loan type, loan amount, interest rate, seller or lender concessions, discount fees, and lender fees. Report includes total cash required plus monthly payment details.

Note: Closing cost report is also available for all Christee modules by accessing the PDF file.

6. Buy or Rent. Explore objective criteria for renting or purchasing a home such as cash required, monthly payment, loan type, tax deductions, potential equity, and return on cash as an investment.

Note. Suitable for consumers and real estate agents.

7. Buy Wait. Develop a in depth report detailing the effects of buying today or delaying a buying decision based on present and future interest rates, property values, monthly payments, required cash, potential equity, tax implications, and future wealth.

Note. Suitable for consumer, agents, and loan officers.

8. Reverse Mortgage. Explore the potential benefits of purchasing a home without a required mortgage payment. This module is based upon the FHA insured reverse mortgage AKA HECM loan. You may enter cash available to see potential purchase price based on available cash.

You may also explore options to purchase a specific price home within a selected location by entering sales price in optional inputs. For Reverse purchase not refinance.

Note. Suitable for consumers, real estate agents, and loan officers.

9. Vacation Explore unique ramifications for buying a 2nd home including estimated tax deductions for both primary and 2nd home. Module identifies areas where non-resident owners’ property taxes are calculated differently.

Note. Suitable for curious consumers, smart agents, and loan officers.

10. Sellers Net. This module develops cost associated with selling a home based upon a selected location. Optional inputs such as close date, property taxes, buyer closing credits, and amortization of loan balance allow for a customized report.

Note. Suitable for curious consumers, agents, and loan officers.

11. Investment Analysis. Develop a comprehensive report for purchasing income producing real estate. Develops Investment ratios suitable for lenders or savvy investors.

Note. Suitable for curious consumers, smart real estate agents, and investment lenders.

12. Home Wealth Analysis. Explore potential wealth is created from homeownership by either reduction in loan balance (amortization) and/or increase in property values (appreciation). You may enter ‘0’ for property appreciation and results will be straight amortization.

Note. Suitable for consumers, agents, and loan officers.